CPS-BLOG-A01

Where Should Sanctions Screening Fit in the Maritime Crew Payroll and Payments Workflow?

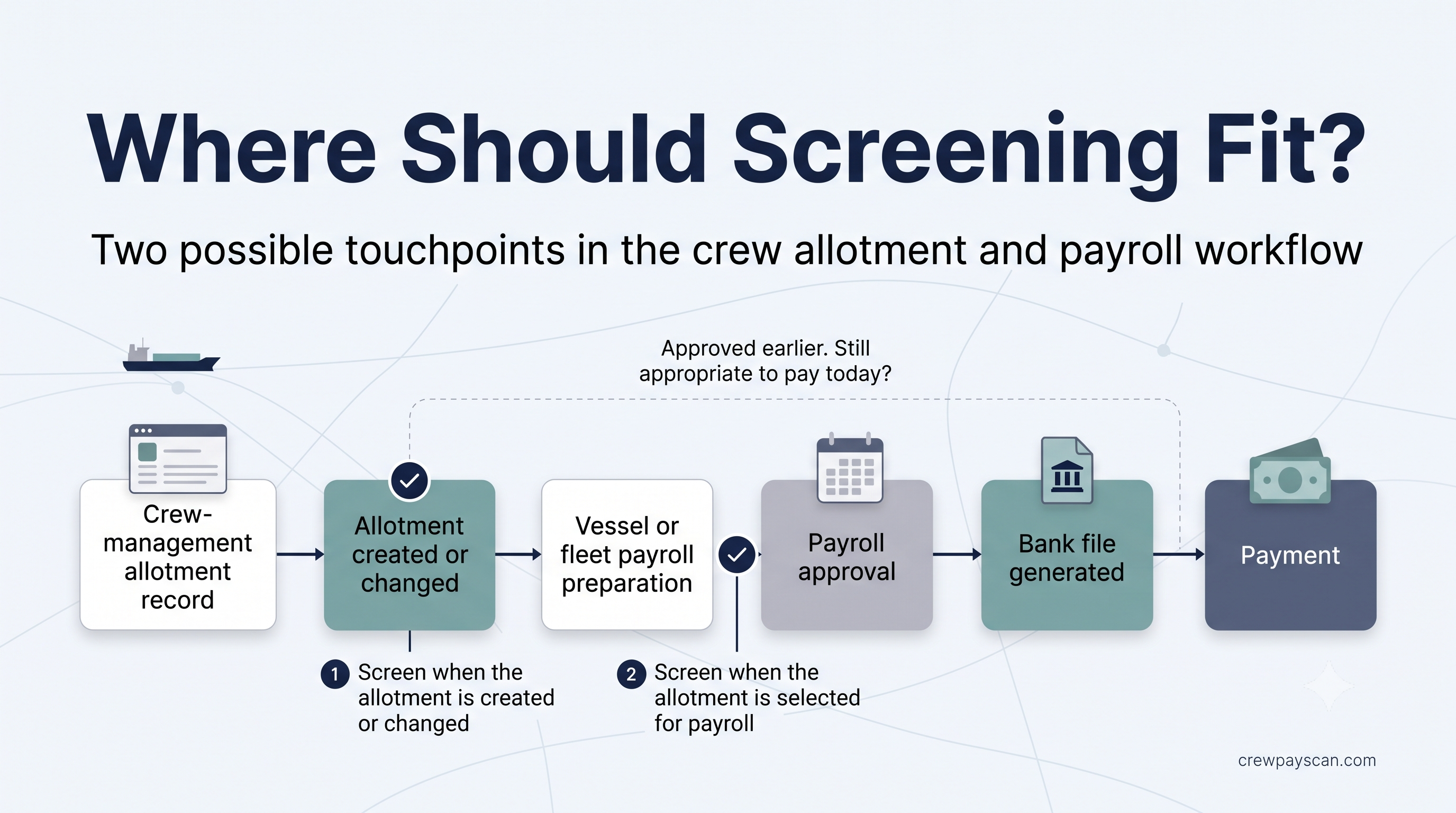

Crew allotment records may remain active across multiple payroll periods, while sanctions information changes over time. This article considers screening when an allotment is created or changed and again when the resulting payment is prepared within a current payment draft.

An allotment was approved six months ago. Is it still safe to pay today?

For a maritime payroll team, the answer may initially appear straightforward. The crew member submitted the instruction, the beneficiary and bank details were reviewed, and the allotment was approved in the company’s crew-management or enterprise system. It may since have contributed to several payroll and payment cycles without any change to the underlying record.

The word “safe,” however, needs to be used carefully. Sanctions screening cannot, by itself, declare that a payment is safe, lawful or ready for release. What it can do is help a team determine whether the information available now presents a possible match that needs to be reviewed before the payment continues.

Here is the distinction that matters: administrative approval of an allotment record and sanctions screening of its beneficiary or receiving bank are related controls, but they are not necessarily the same control.

Even where screening took place when the allotment was first approved, that result reflected the beneficiary and bank details, sanctions sources and matching process available at the time. When the same allotment later produces a payment instruction, the company is making a current payment decision using a record that may have been approved months or even years earlier.

This creates two natural points at which screening might fit:

- When an allotment record is created or its beneficiary or bank details are materially changed.

- When the resulting allotment payment is prepared within a current payment draft.

There is unlikely to be one policy that suits every ship-management or crewing company. But separating these two moments—and separating payroll calculation from payment preparation—makes the underlying workflow much easier to understand.

How approved payroll output becomes allotment payments

Ship-management and crewing companies handling hundreds or thousands of crew generally rely on crew-management software, payroll applications, ERP systems or broader enterprise platforms. The precise arrangement varies considerably. Some companies operate a tightly integrated platform, while others move information between several systems and teams.

Crew allotment records are commonly stored and reused. Once an instruction has been accepted, the system may retain the nominated beneficiary, receiving bank, account information, payment amount or percentage, effective dates and whatever authorisation the company requires.

Many beneficiaries will be spouses, partners, parents, siblings or other family members. It would be inaccurate, though, to assume that the beneficiary population consists only of immediate family. Depending on the crew member’s circumstances and the company’s policies, an allotment may nominate a friend, creditor, mortgage or debt-related recipient, business, institution, charity, representative or another party.

There is nothing inherently unusual about that variety. The operational point is that the company may be making payments to people or organisations that are not its employees and may not have passed through the same onboarding processes as the crew member.

Within payroll, the crew member’s wages, earnings, deductions and active allotments may be calculated for the relevant vessel, fleet or payroll period. A draft payroll is then reviewed and approved through the company’s established process.

What happens next should not automatically be treated as part of the same workflow.

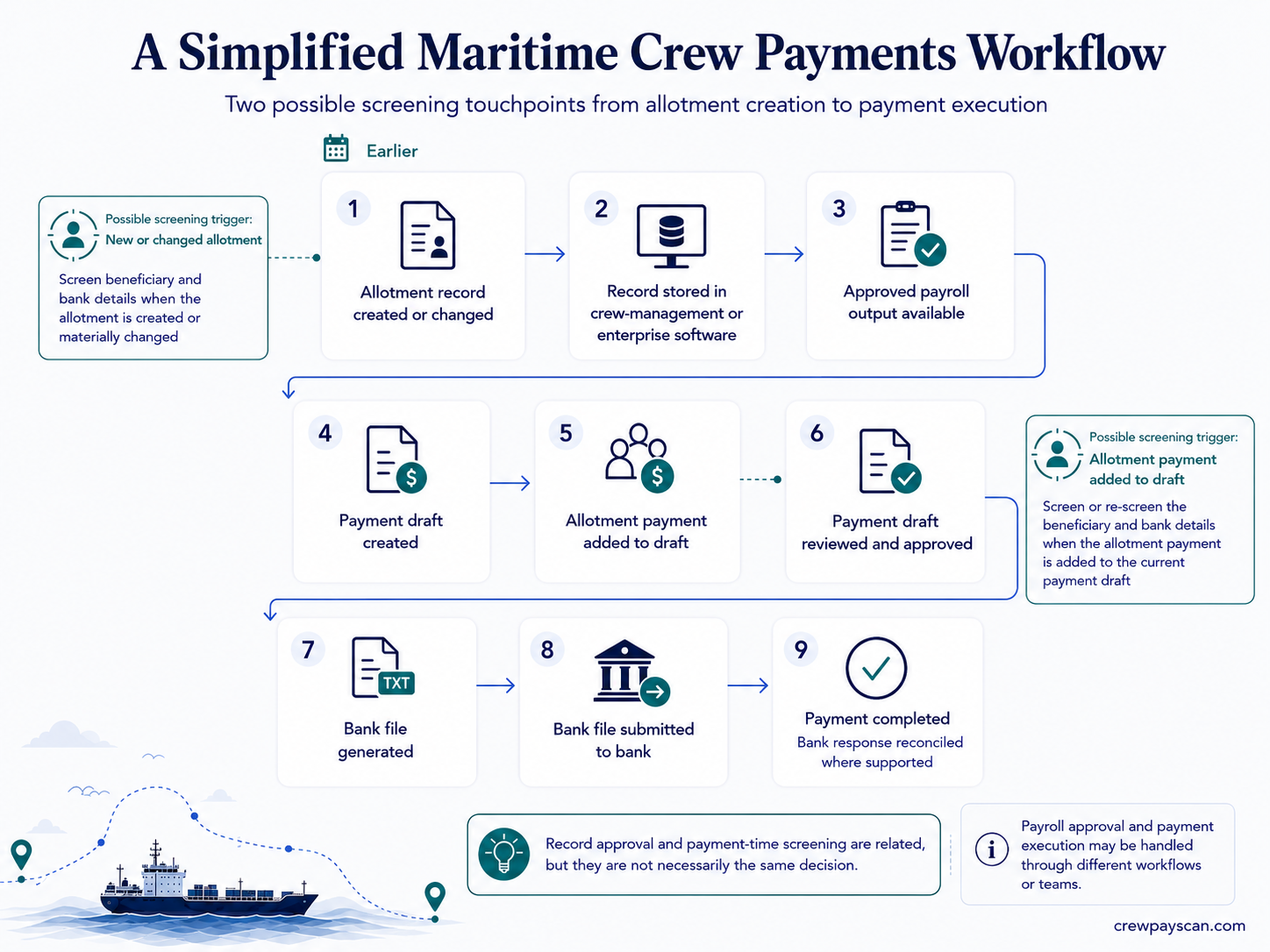

Approved payroll output may become the source for one or more payment drafts. The resulting allotment payments can then be added to the appropriate draft, reviewed and approved before a bank file is generated. The bank file may subsequently be submitted and authorised through the company’s banking process, with payment completion and bank-response reconciliation following where the supporting systems provide that workflow.

A simplified end-to-end sequence might therefore include:

- Opening payroll for a vessel, fleet or payroll period.

- Calculating wages, earnings, deductions and allotment amounts.

- Producing and reviewing a draft payroll.

- Approving and, where applicable, closing payroll.

- Making the approved payroll output available for payment preparation.

- Creating one or more payment drafts and adding the resulting allotment payments.

- Screening or re-screening beneficiary and bank details before the payment draft is approved.

- Approving the payment draft and generating the bank file.

- Submitting and authorising the bank file, completing the payments and reconciling bank responses where supported.

The sequence will not be identical everywhere. Payroll and payments may exist as separate modules within one enterprise platform, as separate applications or as a combination of system-supported and manual processes. Payroll may be handled by crewing or payroll teams, while payment preparation and authorisation may involve finance or treasury.

The important point is not which software boundary a company uses. It is that approving payroll and preparing the resulting payments can involve different records, approvals, responsibilities and points of control.

An approved allotment may continue contributing payment instructions across later payroll periods. The crew member’s payroll is calculated first; the resulting allotment payment may then be added to a payment draft without the underlying allotment record being reviewed from the beginning.

Where the different approvals can diverge

Several related decisions may occur across the allotment, payroll and payments workflows:

- Administrative approval of the allotment record.

- Screening of the beneficiary and receiving-bank details.

- Human review of any possible screening matches.

- Approval of the current payment draft.

When an allotment is created, the administrative review may confirm that the instruction came from the crew member, the required information is complete, supporting authorisation is present, and the arrangement falls within the company’s procedures.

That review establishes whether the allotment record can be accepted and used operationally. It does not necessarily establish whether beneficiary screening or bank-name screening took place.

In some companies, sanctions screening may already be included in the setup or approval process. In others, it may be performed by finance, treasury or compliance, through a payment platform, by a screening provider, or at another stage altogether.

An “approved” status inside a crew-management or payroll system can therefore carry more than one possible meaning. It may mean that the crew member’s instruction is administratively valid. It may mean that screening occurred and was reviewed. Or it may say nothing about screening because that control belongs to another system or team.

Payment-draft approval is a further decision. It concerns the payment instructions being prepared for the current cycle, rather than the administrative validity of the original allotment record.

Unless these meanings are explicit, one team may assume that another has completed a check that was never part of the earlier approval. That is why the distinction is operational rather than merely terminological: it determines what has actually been reviewed, what remains outstanding and who is responsible for the next decision.

Screening moment one: when an allotment is created or changed

The creation of a new crew allotment is a natural point at which to consider screening. The beneficiary and bank details have just entered the company’s workflow, and somebody is already deciding whether the instruction should become active.

Screening at this stage may allow a possible issue to be reviewed before the record begins contributing payments to future payroll periods. If the information is incomplete or ambiguous, it may also be easier to clarify it while the instruction is still being processed.

The same reasoning may apply when an existing allotment changes materially. Replacing the beneficiary is an obvious example, but other changes may also be relevant: a different receiving bank, a replacement bank account, a change in the beneficiary’s name or location, or the reactivation of an old instruction.

A bank-account change needs some care in this context. It may be a sensible trigger for renewed review because the payment instruction has materially changed. That does not necessarily mean the account number itself is screened against a sanctions list. The screening inputs may instead include the beneficiary name, receiving-bank name and other available identifiers, while account validation and payment-detail checks are handled separately.

Not every correction needs to be treated in the same way. Fixing a formatting error is different from redirecting the payment to a new beneficiary or bank. Each company would need to define which changes are material within its own workflow.

Screening at creation or material change gives the organisation a useful starting record. It can show what was checked before the allotment became active, which possible matches appeared and how the reviewer handled them.

But that record answers a time-specific question: what did the available information indicate when this allotment was created or changed?

Screening moment two: when the allotment payment is prepared

The second natural screening moment arises after approved payroll output becomes available and the resulting allotment payment is added to or prepared within the current payment draft.

At that point, the company is no longer deciding whether the underlying allotment record should remain stored and active. It is preparing a current payment instruction for the nominated beneficiary.

Suppose an allotment was properly authorised and screened six months ago. Its beneficiary and bank details remain unchanged, so the crew-management system continues to treat the record as approved. Since the earlier review, however, a sanctions source may have been updated, an alias may have been added, identifying information may have changed, or the company may now be checking an additional source.

A result may also be newly surfaced because the matching configuration or available identifiers have changed. That does not automatically mean the beneficiary or bank has recently become sanctioned. It means that the current screening process has returned information that was not presented in the same way during the earlier review.

Screening during payment-draft preparation allows the team to consider that information before the draft is approved and converted into a bank file.

The precise implementation may vary, but the second touchpoint would normally need to sit after the payment is prepared and before payment-draft approval, bank-file generation and submission. This leaves a practical opportunity to review a possible match while the payment instruction can still be held, clarified or amended through the company’s own process.

Banks and payment providers may perform their own downstream screening. Those controls remain important and operate according to their own procedures. Earlier internal screening does not replace them. It can, however, give the organisation an opportunity to understand and review a possible issue before the payment instruction reaches the bank.

Why a historical approval may not answer a current payment question

Sanctions data changes over time. Parties may be added or removed, and existing entries may acquire new aliases, addresses or other identifying information. A company may also change the sources it checks, obtain better beneficiary information or adjust how potential name matches are identified.

For that reason, an earlier approval and a current screening result should be understood in their proper contexts.

A beneficiary or bank name may have produced no meaningful match when the allotment was first approved and then produce a possible match several months later. The later result does not prove that the first reviewer made the wrong decision. The earlier decision may have been entirely reasonable based on the data and process available at the time.

Nor does a possible name match amount to a confirmed identification. Common names, transliteration, alternative spellings and limited identifying information can produce results that need careful human review. Software can surface those results and preserve the supporting information, but it should not make the compliance judgement on behalf of the reviewer.

The earlier approval records an earlier decision. Preparing a later payment may call for a current decision based on current information.

In that qualified sense, “approved once” should not automatically be treated as “safe forever.”

What a practical screening policy might consider

The appropriate screening policy will depend on how a company organises payroll and payments, how frequently it processes allotments, which systems are involved and who is responsible for reviewing possible matches.

Some companies may decide to screen whenever an allotment is created or materially changed. Others may screen beneficiary and bank details again when the resulting allotment payment is added to a current payment draft, after relevant sanctions-source updates or after a defined period. A combined approach may use more than one trigger and apply different review paths depending on the workflow or information available.

Each approach has operational consequences.

Screening only when a record is created is relatively easy to align with an existing approval process, but that result can become dated. Re-screening every active allotment repeatedly may generate recurring results that teams must review or suppress carefully. Screening during payment-draft preparation provides a more current view, but the check and any required review must be completed before the draft is approved and the bank file is generated.

A practical policy therefore needs to consider both frequency and events. It should define which changes or payment-preparation actions trigger screening, when a previously reviewed result should be shown again, who owns the review and what evidence must be retained.

CrewPayScan is treating these as workflow questions to validate with practitioners, not as universal legal or compliance requirements.

Why historical evidence matters

A screening result is difficult to rely on later if nobody can determine what was checked, which information appeared or why a particular decision was made.

A useful screening history may need to preserve:

- When the screening occurred.

- The beneficiary and bank details checked at that time.

- The sanctions sources used.

- The source version or update date, where available.

- The screening date and dataset or engine version where a formal list snapshot is unavailable.

- The possible matches returned.

- The person who reviewed the result.

- The decision made and the reasoning recorded.

- The allotment or payment event to which the screening related.

- Any later result that differed materially from the earlier screening.

- The information that led to a previous decision being retained or changed.

This history becomes particularly useful when a later payment cycle produces a different result. The reviewer can see whether the same possible match was considered before, whether the beneficiary information or sanctions data has changed, and whether the earlier reasoning still applies.

It may also prevent unnecessary duplication. Teams should not have to reconstruct previous decisions from email threads, spreadsheets or memory. At the same time, an old false-positive decision should not suppress a result indefinitely when the underlying data or circumstances have materially changed.

The record should allow someone reviewing the case later to understand what was checked, what the screening returned and why the reviewer reached the decision recorded at that time. It should not be assumed that retaining these fields automatically satisfies every legal, regulatory or internal evidence requirement.

Where CrewPayScan may fit

CrewPayScan is an early-stage validation project exploring whether a focused workflow layer could support beneficiary and bank-name screening within maritime crew payroll and payment preparation.

The current idea is to work alongside the crew-management, payroll, payments and banking systems a company already uses. The areas being validated include whether such a layer could help teams screen names when an allotment is created or changed and again when the resulting allotment payment is prepared within a current payment draft.

It could also help reviewers examine possible matches, record their decisions and preserve basic evidence showing what was checked and when.

The correct integration point has not been assumed in advance. Different companies may need different triggers, system boundaries and review responsibilities.

Software can make information easier to screen, review and retain. Responsibility for interpreting a possible match and deciding what should happen next remains with the appropriate people within the organisation.

Questions we are validating

We are currently discussing three questions with maritime payroll, crewing, finance, compliance and software professionals:

- When an allotment record is approved in your current process, does that approval include sanctions screening, or does screening happen somewhere else?

- If an approved allotment continues contributing payments across later payroll periods, what event—if any—causes its beneficiary and bank details to be screened again?

- At what point can a possible match still be reviewed properly without creating avoidable disruption to payment-draft approval, bank-file generation or submission?

The answers should help clarify where screening fits, who owns the review and what evidence needs to be preserved once a decision has been made.

Contribute to the private preview

If you work with maritime crew payroll, allotments, payment preparation, crewing operations, finance, compliance or maritime software, you can contribute to the CrewPayScan workflow validation or request access to the private preview.

We are particularly interested in understanding how allotment approval, sanctions screening, approved payroll output and payment-draft preparation interact in real operating environments.

Exploring a similar crew payment screening workflow? Request a private preview to share how your team handles beneficiary and bank-name checks today.